Build-Then-Sell vs. Sell-Then-Build in Malaysia: What It Means for Homebuyers, Developers, and Policymakers

timer

5 minutes read

September 15, 2025

Malaysia’s residential property market is once again in the spotlight following renewed discussions about shifting from the current Sell-Then-Build (STB) model to the Build-Then-Sell (BTS) model. This debate is not new, but it has resurfaced with urgency amid rising cases of delayed and abandoned housing projects, as well as growing buyer dissatisfaction. To understand what’s at stake, it’s important to compare both models, review experiences from regional peers, and evaluate what such a shift would mean for homebuyers, developers, and the government.

Sell-Then-Build (STB): The current dominant model in Malaysia. Buyers purchase a property off-plan and make progressive payments (via housing loans) while the project is under construction.

Build-Then-Sell (BTS): Buyers only pay when the property is completed and ready for occupancy. Developers bear the financing risk until delivery.

80% of housing is government-built (HDB): This means the bulk of citizens are protected, and the risks of STB only affect a small private market.

Strict regulation: Developers must hold buyer payments in escrow, progressive payments are tied tightly to construction milestones, and the government enforces harsh penalties for delays.

Impact: Singapore balances STB to boost housing supply while minimizing risks, with long-term stability backed by state control.

Impact: This model has boosted buyer confidence, but reduced participation of smaller developers. The market consolidated around larger, financially stronger players.

Millions of buyers left without completed homes.

Banks heavily exposed to non-performing loans.

Government forced into costly bailouts, erasing the earlier GDP gains.

Impact: Short-term GDP boost, long-term social crisis. The collapse undermined trust, left many families homeless, and required taxpayer-funded interventions.

For Homebuyers

STB Pros:

Lower entry cost (progressive payments).

Early access to price appreciation.

STB Cons:

High risk of delays or project abandonment.

Buyers service loans even before moving in.

BTS Pros:

Strong buyer protection — pay only for completed homes.

Higher confidence in quality and delivery.

BTS Cons:

Higher upfront property prices as developers carry financing costs.

Fewer choices in early-stage projects.

STB Pros:

Easier access to financing via buyer payments.

Lower capital requirement upfront.

STB Cons:

Exposed to reputational damage if projects are delayed.

Dependence on consistent sales to fund construction.

BTS Pros:

Stronger trust and long-term brand building.

More sustainable demand (buyers purchase when ready).

BTS Cons:

Heavy reliance on bank/project financing.

Smaller developers may struggle to survive.

Malaysia has experienced over 500 abandoned housing projects over the past decades, eroding buyer confidence. Policymakers believe BTS could restore trust, but developers warn it could shrink supply and limit participation from smaller firms. The key question is whether Malaysia’s financial system and government safeguards are strong enough to support a BTS transition.

STB Short-Term: Drives GDP growth by fueling construction and speculative demand. Creates wealth effect for early buyers and boosts ancillary industries (cement, steel, finance).

STB Long-Term: If projects fail, systemic risks emerge — homeowners stranded, banks exposed, government forced into bailouts (China’s Evergrande). Net effect: earlier GDP growth erased by long-term social and economic instability.

BTS Short-Term: Slows GDP contribution from property. Developers face financing bottlenecks, and supply dips initially.

BTS Long-Term: Builds sustainable housing ecosystems. Stronger buyer trust, reduced systemic risks, and healthier, demand-driven growth.

Singapore: STB works only because of disproportionate government housing (HDB) covering 80% of citizens, plus strict escrow and regulatory oversight. Without such conditions, STB would expose buyers to huge risks.

Australia: BTS creates stability but at the cost of excluding smaller players. Market consolidates, but buyers are safe.

China: STB drove short-term GDP, but Evergrande showed how its collapse can wipe out decades of trust, wealth, and stability. A cautionary tale for Malaysia.

Homebuyers: Likely to benefit most from BTS through better protection and confidence, though affordability may be challenged in the short term.

Developers: Larger, well-capitalized developers will thrive under BTS, while smaller players may struggle without new financing avenues.

Government: Must step in with support mechanisms — such as development banks, project financing guarantees, or a hybrid STB-BTS system — to ensure a smooth transition.

Q1: What is the difference between Sell-Then-Build (STB) and Build-Then-Sell (BTS)?

STB allows buyers to pay progressively before the home is completed, while BTS requires full payment only after completion.

Q2: Why is Malaysia considering the BTS model?

To protect buyers from abandoned projects and restore confidence in the property market.

Q3: Will property prices increase under BTS?

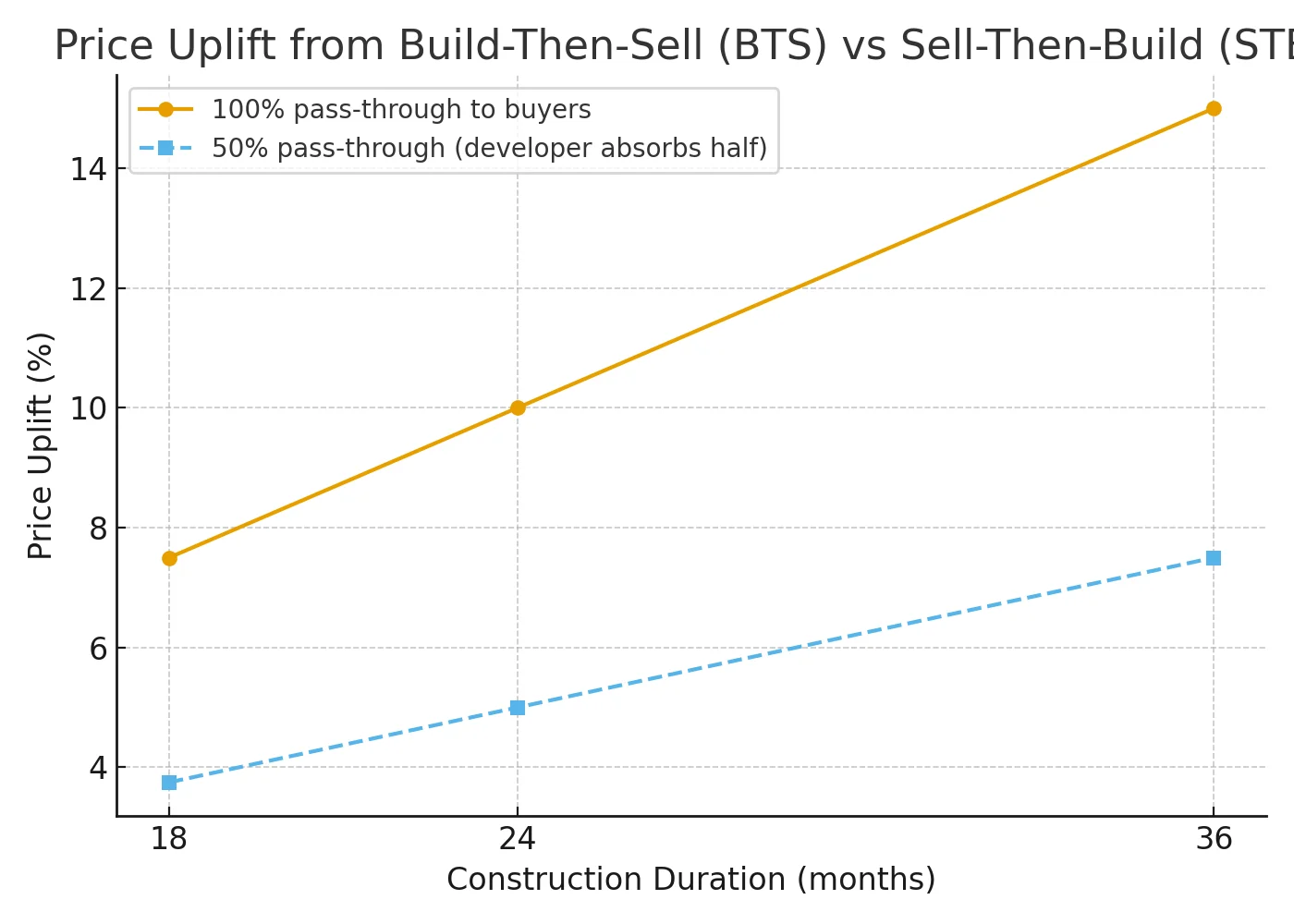

Yes, developers are expected to pass on financing costs, with estimates ranging from 5% to 20% increases.

Q4: How will BTS affect small developers?

Smaller developers may struggle to raise upfront capital, leading to market consolidation around larger players.

Q5: Which countries already use BTS?

Australia predominantly uses BTS, while Singapore and China use hybrids or are shifting towards stricter buyer protection models.

Q6: What are the long-term risks of STB?

As shown by China’s Evergrande case, STB can create systemic risks — unfinished homes, bank failures, and costly government bailouts — undermining social and economic stability.

The Two Models Explained

Sell-Then-Build (STB): The current dominant model in Malaysia. Buyers purchase a property off-plan and make progressive payments (via housing loans) while the project is under construction.

Build-Then-Sell (BTS): Buyers only pay when the property is completed and ready for occupancy. Developers bear the financing risk until delivery.

International Comparisons

Singapore – STB with Strong Safeguards

Singapore operates a hybrid STB system, but it works due to two critical factors:80% of housing is government-built (HDB): This means the bulk of citizens are protected, and the risks of STB only affect a small private market.

Strict regulation: Developers must hold buyer payments in escrow, progressive payments are tied tightly to construction milestones, and the government enforces harsh penalties for delays.

Impact: Singapore balances STB to boost housing supply while minimizing risks, with long-term stability backed by state control.

Australia – Predominantly BTS

Australia’s residential market favors BTS, especially for landed homes and apartments. Buyers pay deposits and settle the balance only upon completion.Impact: This model has boosted buyer confidence, but reduced participation of smaller developers. The market consolidated around larger, financially stronger players.

China – STB Gone Wrong (Evergrande)

China historically relied on STB, which fueled rapid GDP growth as developers used pre-sales to fund aggressive expansions. However, the Evergrande crisis revealed the systemic risks:Millions of buyers left without completed homes.

Banks heavily exposed to non-performing loans.

Government forced into costly bailouts, erasing the earlier GDP gains.

Impact: Short-term GDP boost, long-term social crisis. The collapse undermined trust, left many families homeless, and required taxpayer-funded interventions.

Indonesia & Thailand – STB with Weak Oversight

Both markets rely on STB, but weak enforcement has led to frequent project delays and abandoned developments. Buyer protection remains inconsistent.Pros and Cons of Each Model

For Homebuyers

STB Pros:

Lower entry cost (progressive payments).

Early access to price appreciation.

STB Cons:

High risk of delays or project abandonment.

Buyers service loans even before moving in.

BTS Pros:

Strong buyer protection — pay only for completed homes.

Higher confidence in quality and delivery.

BTS Cons:

Higher upfront property prices as developers carry financing costs.

Fewer choices in early-stage projects.

For Developers

STB Pros:

Easier access to financing via buyer payments.

Lower capital requirement upfront.

STB Cons:

Exposed to reputational damage if projects are delayed.

Dependence on consistent sales to fund construction.

BTS Pros:

Stronger trust and long-term brand building.

More sustainable demand (buyers purchase when ready).

BTS Cons:

Heavy reliance on bank/project financing.

Smaller developers may struggle to survive.

The Malaysian Dilemma

Malaysia has experienced over 500 abandoned housing projects over the past decades, eroding buyer confidence. Policymakers believe BTS could restore trust, but developers warn it could shrink supply and limit participation from smaller firms. The key question is whether Malaysia’s financial system and government safeguards are strong enough to support a BTS transition.

Data-Driven Impact Analysis

1. Price Impact Scenarios

2. Supply-Side Impact

Short-Term vs Long-Term and Social Impacts

STB Short-Term: Drives GDP growth by fueling construction and speculative demand. Creates wealth effect for early buyers and boosts ancillary industries (cement, steel, finance).

STB Long-Term: If projects fail, systemic risks emerge — homeowners stranded, banks exposed, government forced into bailouts (China’s Evergrande). Net effect: earlier GDP growth erased by long-term social and economic instability.

BTS Short-Term: Slows GDP contribution from property. Developers face financing bottlenecks, and supply dips initially.

BTS Long-Term: Builds sustainable housing ecosystems. Stronger buyer trust, reduced systemic risks, and healthier, demand-driven growth.

Lessons from Peers

Singapore: STB works only because of disproportionate government housing (HDB) covering 80% of citizens, plus strict escrow and regulatory oversight. Without such conditions, STB would expose buyers to huge risks.

Australia: BTS creates stability but at the cost of excluding smaller players. Market consolidates, but buyers are safe.

China: STB drove short-term GDP, but Evergrande showed how its collapse can wipe out decades of trust, wealth, and stability. A cautionary tale for Malaysia.

What This Could Mean for Malaysia

Homebuyers: Likely to benefit most from BTS through better protection and confidence, though affordability may be challenged in the short term.

Developers: Larger, well-capitalized developers will thrive under BTS, while smaller players may struggle without new financing avenues.

Government: Must step in with support mechanisms — such as development banks, project financing guarantees, or a hybrid STB-BTS system — to ensure a smooth transition.

FAQs

Q1: What is the difference between Sell-Then-Build (STB) and Build-Then-Sell (BTS)?

STB allows buyers to pay progressively before the home is completed, while BTS requires full payment only after completion.

Q2: Why is Malaysia considering the BTS model?

To protect buyers from abandoned projects and restore confidence in the property market.

Q3: Will property prices increase under BTS?

Yes, developers are expected to pass on financing costs, with estimates ranging from 5% to 20% increases.

Q4: How will BTS affect small developers?

Smaller developers may struggle to raise upfront capital, leading to market consolidation around larger players.

Q5: Which countries already use BTS?

Australia predominantly uses BTS, while Singapore and China use hybrids or are shifting towards stricter buyer protection models.

Q6: What are the long-term risks of STB?

As shown by China’s Evergrande case, STB can create systemic risks — unfinished homes, bank failures, and costly government bailouts — undermining social and economic stability.