Sunway's RM11 Billion Bid for IJM Collapses — What Property Buyers Need to Know

timer

8 minutes read

April 8, 2026

Malaysia's biggest corporate story of early 2026 is over. On 6 April 2026, Sunway Berhad's attempted RM11 billion takeover of IJM Corporation officially lapsed — rejected by the very shareholders it needed most. If you've been tracking both developers as a homebuyer or property investor, here's a clear breakdown of what happened, why it failed, and what it means for you.

The proposed deal was a conditional voluntary takeover offer (VTO) by Sunway Berhad to acquire all shares in IJM Corporation Berhad at RM3.15 per share — valuing IJM at roughly RM11 billion in total.

Sunway announced the offer on 12 January 2026. The structure was primarily a share swap: for every IJM share you held, Sunway offered you RM0.315 in cash and approximately 0.501 new Sunway shares. In practice, 90% of the deal was paid in Sunway stock, not cash.

The strategic ambition was significant. A merged Sunway-IJM would have become Malaysia's largest property and construction conglomerate — surpassing Gamuda — with a combined gross development value of RM118 billion, a construction order book of RM14.8 billion, and total assets approaching RM57 billion.

For Malaysian property buyers, both names matter. Sunway develops townships in Klang Valley, Penang, and Johor. IJM Land builds across the same corridors, including its flagship Rimbayu township in Shah Alam and projects in Penang, Seremban, and Johor Bahru.

This was the core issue. Two independent valuers appointed under Securities Commission rules both concluded Sunway's offer was nowhere near fair value.

M&A Securities valued IJM at RM5.84 to RM6.48 per share — meaning the RM3.15 offer represented a 46 to 51% discount to what the company was actually worth.

Rothschild & Co Malaysia valued IJM at RM4.80 to RM5.63 per share — still a 34 to 44% discount.

Both advisers formally concluded the offer was "not fair and not reasonable" and recommended shareholders reject it.

To put that in perspective: IJM's toll highway division alone — which includes the Sungai Besi Expressway and the Kajang-Seremban Highway — was valued at RM3.83 to RM4.55 billion by itself. Sunway was essentially asking to buy the entire company for less than the value of one of its divisions.

Sunway argued its own track record justified the price — pointing out IJM's 10-year total shareholder return was negative 9% versus Sunway's 387% — but critics responded that if the synergies were real, the offer should have reflected some of that upside for IJM shareholders rather than capturing it entirely for Sunway.

IJM's two largest shareholders were EPF (Employees Provident Fund) and PNB (Permodalan Nasional Bhd) — between them holding approximately 34% of IJM shares.

PNB rejected the offer on 16 March 2026.

EPF — holding the largest single stake at 20.52% — rejected on 27 March 2026, stating the price did not reflect IJM's intrinsic value.

With EPF and PNB locked against the deal, reaching the required 50% acceptance threshold was mathematically near-impossible. By the time the offer closed on 6 April, only 33.43% of IJM shareholders had accepted — well short of the finish line.

The 90%-shares, 10%-cash structure meant IJM shareholders weren't getting a clean exit. They were being asked to convert their IJM holdings into a minority position in an enlarged Sunway — at a steep implied discount. For EPF and PNB, whose mandate is to protect long-term member interests, that trade-off simply didn't stack up.

The deal attracted political commentary alongside financial scrutiny. Some politicians and commentators raised concerns that the takeover — by a company controlled by ethnic Chinese billionaire Tan Sri Jeffrey Cheah — would reduce Bumiputera equity exposure to strategic national assets like toll highways and ports.

Sunway co-chairman Datuk Seri Idris Jala publicly rejected these characterisations. Cheah himself acknowledged that GLICs were initially receptive after the announcement but that sentiment shifted after social media commentary along racial lines.

Separately, the Malaysian Anti-Corruption Commission (MACC) confirmed in early March that it had opened three investigation papers connected to IJM — involving governance issues around public funds, alleged bribery linked to an IJM project, and alleged money laundering. Sunway was formally cleared by MACC on 25–26 March. IJM clarified the investigations were focused on specific individuals, not the company itself.

IJM's CEO Datuk Lee Chun Fai responded quickly. With the takeover threat removed, IJM has committed to an accelerated standalone strategy:

Listing the construction division separately on Bursa Malaysia

Spinning off the highway concession assets (including Sungai Besi and Kajang-Seremban) within two to three years

Rationalising its India portfolio

Potentially listing its industrial concrete operations

The thesis is simple: IJM as a conglomerate trades at a discount because markets struggle to value four different businesses under one roof. Separating them allows each to be priced on its own merits. IJM also holds a record RM17.3 billion construction order book and cash reserves of RM2.3 billion, and has recently won data centre contracts worth over RM1.9 billion.

The risk: execution. As analysts note, IJM now carries the burden of proving these plans are credible — and delivering within the promised timeframe.

Sunway walks away with its balance sheet intact. The failed bid didn't cost it cash beyond advisory fees. Analysts expect Sunway to continue pursuing acquisitions — its appetite for inorganic growth is clearly intact. Meanwhile, Sunway's other corporate events in the same period were positive: the listing of Sunway Healthcare Holdings debuted at roughly RM16 billion market capitalisation with a strong first-day gain, and its MCL Land acquisition in Singapore more than doubled its Singapore property exposure.

Both developers continue building. The failed takeover does not affect either company's ongoing property launches, ongoing construction projects, or unit deliveries. Homebuyers who have signed SPAs with IJM Land or Sunway Property are unaffected.

IJM Land may get more investor attention. With a concrete plan to unlock value — including listing divisions and spinning off assets — IJM Land's parent has committed to restructuring that could improve transparency and focus. That could be positive for the brand's long-term health.

Sunway remains one of Malaysia's most active developers. With property launches guided at RM4.2 billion for FY2026 and its Singapore exposure now significantly expanded, Sunway's pipeline remains robust. Projects like [Sunway SPK 3 Harmoni in KL] are ongoing.

The deal's collapse is a reminder that corporate valuations matter. GLICs like EPF are the custodians of Malaysians' retirement savings. Their rejection of the RM3.15 offer — at what independent advisers calculated was a 34–51% discount to intrinsic value — is a signal that Malaysia's institutional investment community is becoming more sophisticated about protecting long-term value. That's broadly good news for Malaysian capital markets.

If you want to explore new property projects from either developer or connect with an agent who knows their launches, [browse verified MRB listings on our property map] or [visit the MRB homepage] to connect with a verified agent near you.

Sunway's RM11 billion bid for IJM collapsed on 6 April 2026, securing only 33.43% acceptance against a required 50%

Independent advisers valued IJM at RM4.80–RM6.48 per share — the RM3.15 offer was a 34–51% discount to intrinsic value

EPF (20.52%) and PNB (13.5%) rejected the offer, effectively killing the deal

IJM now plans to list its construction arm and spin off highway concessions as a standalone value-creation strategy

Sunway remains financially strong and is expected to pursue other acquisitions

Neither developer's ongoing property launches or homebuyer commitments are affected

[Browse new property launches on the MRB map]

[Sunway SPK 3 Harmoni — a Sunway residential project in Kuala Lumpur]

Q: Does the failed Sunway-IJM merger affect my property purchase from either developer? A: No. A takeover offer at the corporate/holding company level does not affect individual property purchases, ongoing construction projects, or signed Sale and Purchase Agreements. Both Sunway Property and IJM Land continue to operate independently and normally.

Q: Why did Sunway's RM3.15 offer fail when it was a 14.5% premium to IJM's market price? A: Market price and intrinsic value are different things. IJM's independent advisers calculated its intrinsic value at RM4.80–RM6.48 per share using sum-of-parts analysis — meaning the market price at the time was itself trading at a significant discount to fair value. A 14.5% premium on an undervalued stock can still be a deeply inadequate offer.

Q: What is EPF's role in Malaysian corporate takeovers? A: EPF (Employees Provident Fund) is Malaysia's national pension fund and one of the country's largest institutional investors. It holds significant stakes in many Bursa-listed companies. As a major shareholder, EPF votes on corporate actions including takeovers. Its decision to reject Sunway's offer — citing intrinsic value concerns — was decisive in killing the deal.

Q: What is a Voluntary Takeover Offer (VTO)? A: A VTO is an offer by one company to purchase shares in another company from existing shareholders at a stated price, subject to conditions such as a minimum acceptance level. Under Malaysian securities law, if the offer reaches a 90% acceptance threshold, the acquirer can compulsorily acquire remaining shares. Below 50%, the offer typically lapses — as happened with Sunway's bid for IJM.

Q: Will Sunway try again to acquire IJM? A: Under Malaysian takeover rules, a failed bidder is generally subject to a cooling-off period before it can make another offer for the same company. Sunway has not publicly indicated any intention to re-bid. Analysts expect Sunway to focus on other acquisition targets and organic growth.

Written by MRB Editorial Team | Last reviewed April 2026

What Was the Sunway-IJM Deal?

The proposed deal was a conditional voluntary takeover offer (VTO) by Sunway Berhad to acquire all shares in IJM Corporation Berhad at RM3.15 per share — valuing IJM at roughly RM11 billion in total.

Sunway announced the offer on 12 January 2026. The structure was primarily a share swap: for every IJM share you held, Sunway offered you RM0.315 in cash and approximately 0.501 new Sunway shares. In practice, 90% of the deal was paid in Sunway stock, not cash.

The strategic ambition was significant. A merged Sunway-IJM would have become Malaysia's largest property and construction conglomerate — surpassing Gamuda — with a combined gross development value of RM118 billion, a construction order book of RM14.8 billion, and total assets approaching RM57 billion.

For Malaysian property buyers, both names matter. Sunway develops townships in Klang Valley, Penang, and Johor. IJM Land builds across the same corridors, including its flagship Rimbayu township in Shah Alam and projects in Penang, Seremban, and Johor Bahru.

Why Did the Deal Fail?

1. The price was too low — by a wide margin

This was the core issue. Two independent valuers appointed under Securities Commission rules both concluded Sunway's offer was nowhere near fair value.

M&A Securities valued IJM at RM5.84 to RM6.48 per share — meaning the RM3.15 offer represented a 46 to 51% discount to what the company was actually worth.

Rothschild & Co Malaysia valued IJM at RM4.80 to RM5.63 per share — still a 34 to 44% discount.

Both advisers formally concluded the offer was "not fair and not reasonable" and recommended shareholders reject it.

To put that in perspective: IJM's toll highway division alone — which includes the Sungai Besi Expressway and the Kajang-Seremban Highway — was valued at RM3.83 to RM4.55 billion by itself. Sunway was essentially asking to buy the entire company for less than the value of one of its divisions.

Sunway argued its own track record justified the price — pointing out IJM's 10-year total shareholder return was negative 9% versus Sunway's 387% — but critics responded that if the synergies were real, the offer should have reflected some of that upside for IJM shareholders rather than capturing it entirely for Sunway.

2. Government-linked funds said no

IJM's two largest shareholders were EPF (Employees Provident Fund) and PNB (Permodalan Nasional Bhd) — between them holding approximately 34% of IJM shares.

PNB rejected the offer on 16 March 2026.

EPF — holding the largest single stake at 20.52% — rejected on 27 March 2026, stating the price did not reflect IJM's intrinsic value.

With EPF and PNB locked against the deal, reaching the required 50% acceptance threshold was mathematically near-impossible. By the time the offer closed on 6 April, only 33.43% of IJM shareholders had accepted — well short of the finish line.

3. The share-swap structure made it unattractive

The 90%-shares, 10%-cash structure meant IJM shareholders weren't getting a clean exit. They were being asked to convert their IJM holdings into a minority position in an enlarged Sunway — at a steep implied discount. For EPF and PNB, whose mandate is to protect long-term member interests, that trade-off simply didn't stack up.

4. Racial politics and MACC added noise

The deal attracted political commentary alongside financial scrutiny. Some politicians and commentators raised concerns that the takeover — by a company controlled by ethnic Chinese billionaire Tan Sri Jeffrey Cheah — would reduce Bumiputera equity exposure to strategic national assets like toll highways and ports.

Sunway co-chairman Datuk Seri Idris Jala publicly rejected these characterisations. Cheah himself acknowledged that GLICs were initially receptive after the announcement but that sentiment shifted after social media commentary along racial lines.

Separately, the Malaysian Anti-Corruption Commission (MACC) confirmed in early March that it had opened three investigation papers connected to IJM — involving governance issues around public funds, alleged bribery linked to an IJM project, and alleged money laundering. Sunway was formally cleared by MACC on 25–26 March. IJM clarified the investigations were focused on specific individuals, not the company itself.

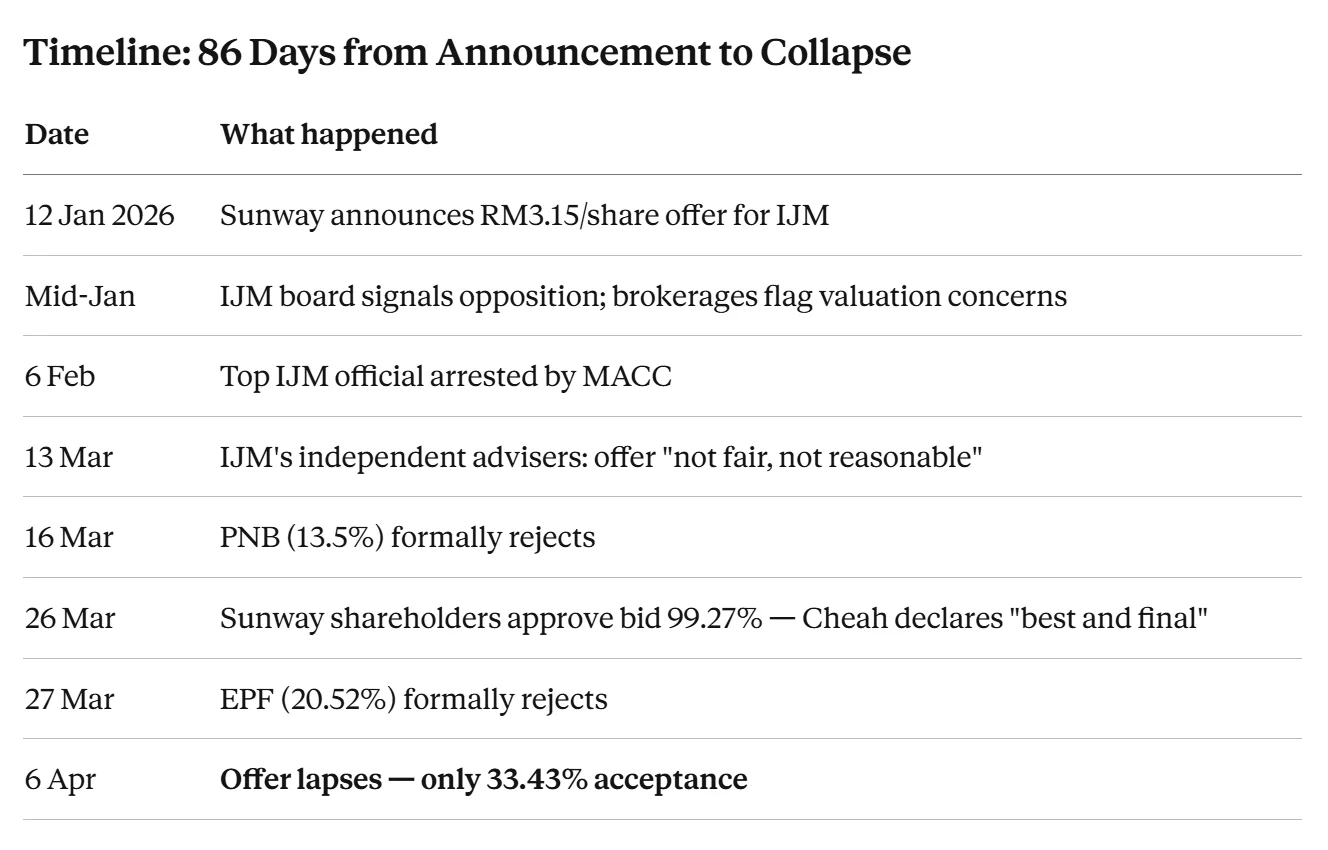

Timeline: 86 Days from Announcement to Collapse

What Happens to Both Companies Now?

IJM: Unlocking value on its own terms

IJM's CEO Datuk Lee Chun Fai responded quickly. With the takeover threat removed, IJM has committed to an accelerated standalone strategy:

Listing the construction division separately on Bursa Malaysia

Spinning off the highway concession assets (including Sungai Besi and Kajang-Seremban) within two to three years

Rationalising its India portfolio

Potentially listing its industrial concrete operations

The thesis is simple: IJM as a conglomerate trades at a discount because markets struggle to value four different businesses under one roof. Separating them allows each to be priced on its own merits. IJM also holds a record RM17.3 billion construction order book and cash reserves of RM2.3 billion, and has recently won data centre contracts worth over RM1.9 billion.

The risk: execution. As analysts note, IJM now carries the burden of proving these plans are credible — and delivering within the promised timeframe.

Sunway: Still growing, still acquisitive

Sunway walks away with its balance sheet intact. The failed bid didn't cost it cash beyond advisory fees. Analysts expect Sunway to continue pursuing acquisitions — its appetite for inorganic growth is clearly intact. Meanwhile, Sunway's other corporate events in the same period were positive: the listing of Sunway Healthcare Holdings debuted at roughly RM16 billion market capitalisation with a strong first-day gain, and its MCL Land acquisition in Singapore more than doubled its Singapore property exposure.

What Does This Mean for Malaysian Property Buyers?

Both developers continue building. The failed takeover does not affect either company's ongoing property launches, ongoing construction projects, or unit deliveries. Homebuyers who have signed SPAs with IJM Land or Sunway Property are unaffected.

IJM Land may get more investor attention. With a concrete plan to unlock value — including listing divisions and spinning off assets — IJM Land's parent has committed to restructuring that could improve transparency and focus. That could be positive for the brand's long-term health.

Sunway remains one of Malaysia's most active developers. With property launches guided at RM4.2 billion for FY2026 and its Singapore exposure now significantly expanded, Sunway's pipeline remains robust. Projects like [Sunway SPK 3 Harmoni in KL] are ongoing.

The deal's collapse is a reminder that corporate valuations matter. GLICs like EPF are the custodians of Malaysians' retirement savings. Their rejection of the RM3.15 offer — at what independent advisers calculated was a 34–51% discount to intrinsic value — is a signal that Malaysia's institutional investment community is becoming more sophisticated about protecting long-term value. That's broadly good news for Malaysian capital markets.

If you want to explore new property projects from either developer or connect with an agent who knows their launches, [browse verified MRB listings on our property map] or [visit the MRB homepage] to connect with a verified agent near you.

Key Takeaways

Sunway's RM11 billion bid for IJM collapsed on 6 April 2026, securing only 33.43% acceptance against a required 50%

Independent advisers valued IJM at RM4.80–RM6.48 per share — the RM3.15 offer was a 34–51% discount to intrinsic value

EPF (20.52%) and PNB (13.5%) rejected the offer, effectively killing the deal

IJM now plans to list its construction arm and spin off highway concessions as a standalone value-creation strategy

Sunway remains financially strong and is expected to pursue other acquisitions

Neither developer's ongoing property launches or homebuyer commitments are affected

Related Reading

[Browse new property launches on the MRB map]

[Sunway SPK 3 Harmoni — a Sunway residential project in Kuala Lumpur]

Frequently Asked Questions

Q: Does the failed Sunway-IJM merger affect my property purchase from either developer? A: No. A takeover offer at the corporate/holding company level does not affect individual property purchases, ongoing construction projects, or signed Sale and Purchase Agreements. Both Sunway Property and IJM Land continue to operate independently and normally.

Q: Why did Sunway's RM3.15 offer fail when it was a 14.5% premium to IJM's market price? A: Market price and intrinsic value are different things. IJM's independent advisers calculated its intrinsic value at RM4.80–RM6.48 per share using sum-of-parts analysis — meaning the market price at the time was itself trading at a significant discount to fair value. A 14.5% premium on an undervalued stock can still be a deeply inadequate offer.

Q: What is EPF's role in Malaysian corporate takeovers? A: EPF (Employees Provident Fund) is Malaysia's national pension fund and one of the country's largest institutional investors. It holds significant stakes in many Bursa-listed companies. As a major shareholder, EPF votes on corporate actions including takeovers. Its decision to reject Sunway's offer — citing intrinsic value concerns — was decisive in killing the deal.

Q: What is a Voluntary Takeover Offer (VTO)? A: A VTO is an offer by one company to purchase shares in another company from existing shareholders at a stated price, subject to conditions such as a minimum acceptance level. Under Malaysian securities law, if the offer reaches a 90% acceptance threshold, the acquirer can compulsorily acquire remaining shares. Below 50%, the offer typically lapses — as happened with Sunway's bid for IJM.

Q: Will Sunway try again to acquire IJM? A: Under Malaysian takeover rules, a failed bidder is generally subject to a cooling-off period before it can make another offer for the same company. Sunway has not publicly indicated any intention to re-bid. Analysts expect Sunway to focus on other acquisition targets and organic growth.

Written by MRB Editorial Team | Last reviewed April 2026