Malaysia Property Market 2026: What the Data Is Really Telling Us

timer

11 minutes read

April 3, 2026

Malaysia's property market is navigating one of its most complex environments in a decade. The economy is performing well, developers posted record sales in 2025, and a generational infrastructure project is taking shape in Johor. But transaction volumes have fallen sharply, loan rejections are blocking a significant share of buyers, unsold stock is building, and a geopolitical storm — the Iran conflict, US tariffs, and oil above $100 per barrel — has arrived at the worst possible moment.

This is not a market in freefall. But it is a market under real, structural pressure. Here is what the data shows.

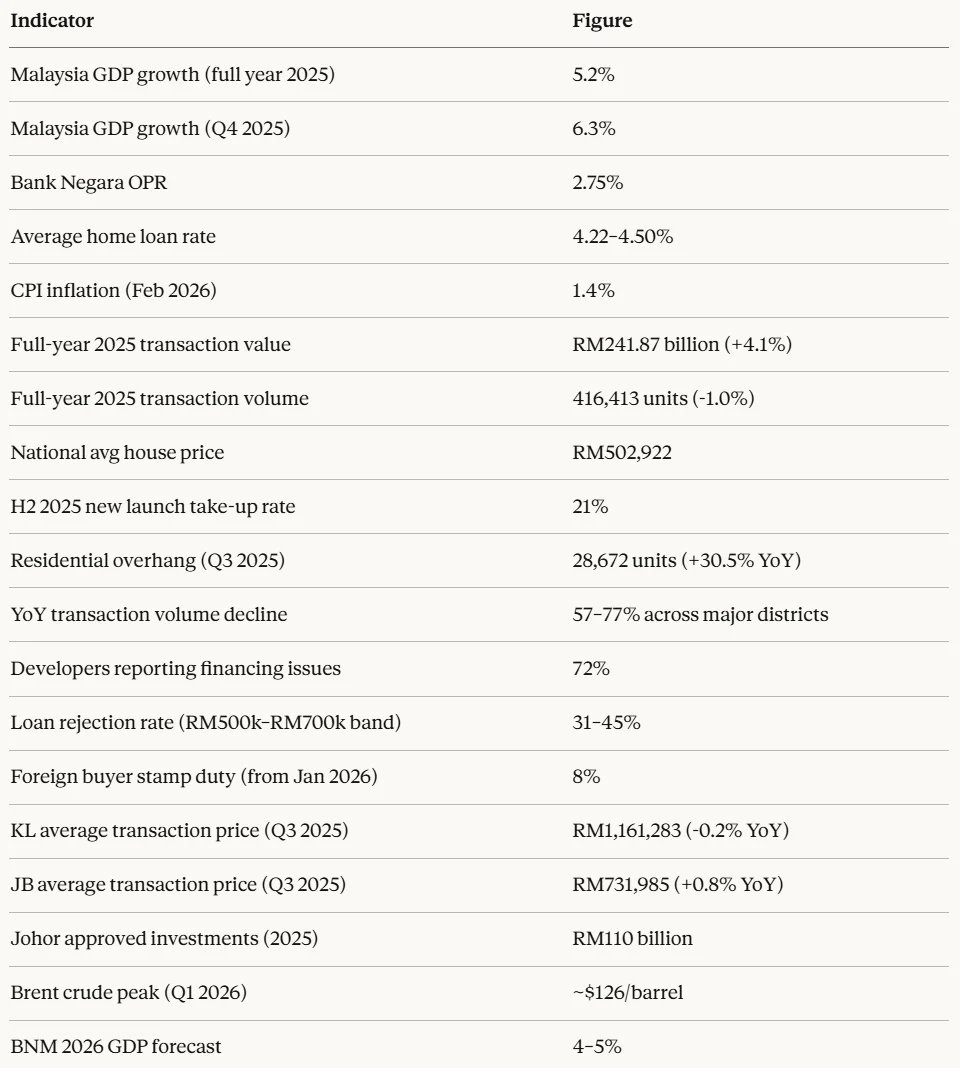

Malaysia's GDP grew 6.3% in Q4 2025 — the strongest quarter in three years — and full-year 2025 growth came in at 5.2%, beating the government's own forecast. Unemployment fell to 2.9%, a decade low. The ringgit strengthened to its best level against the US dollar since 2018.

Bank Negara Malaysia held the Overnight Policy Rate at 2.75% through both its January and March 2026 meetings. Home loan rates for well-qualified buyers sit at 4.22–4.50% for conventional financing, and 3.95–4.15% for Islamic home loans. Inflation remains subdued at 1.4% as of February 2026.

On paper, these are conditions that should support a healthy property market. The friction is structural, not macroeconomic.

The full-year 2025 NAPIC Property Market Report, released on 19 March 2026, confirmed that Malaysia's property market delivered value growth but volume decline. Total transaction value rose to RM241.87 billion — up 4.1% — on 416,413 transactions, down 1% year-on-year.

That headline figure, however, masks diverging trends. The national house price index grew just 2.6% for the full year, with the average transaction price reaching RM502,922. But by Q3 2025, the index had slipped 1.46% quarter-on-quarter — the first such quarterly decline since Q3 2021. Adjusted for inflation, house prices fell in real terms.

The segment driving headline value growth was industrial property, which surged 21.3% in value — powered by data centre land deals and logistics demand. Residential property, which most Malaysians actually care about, told a different story.

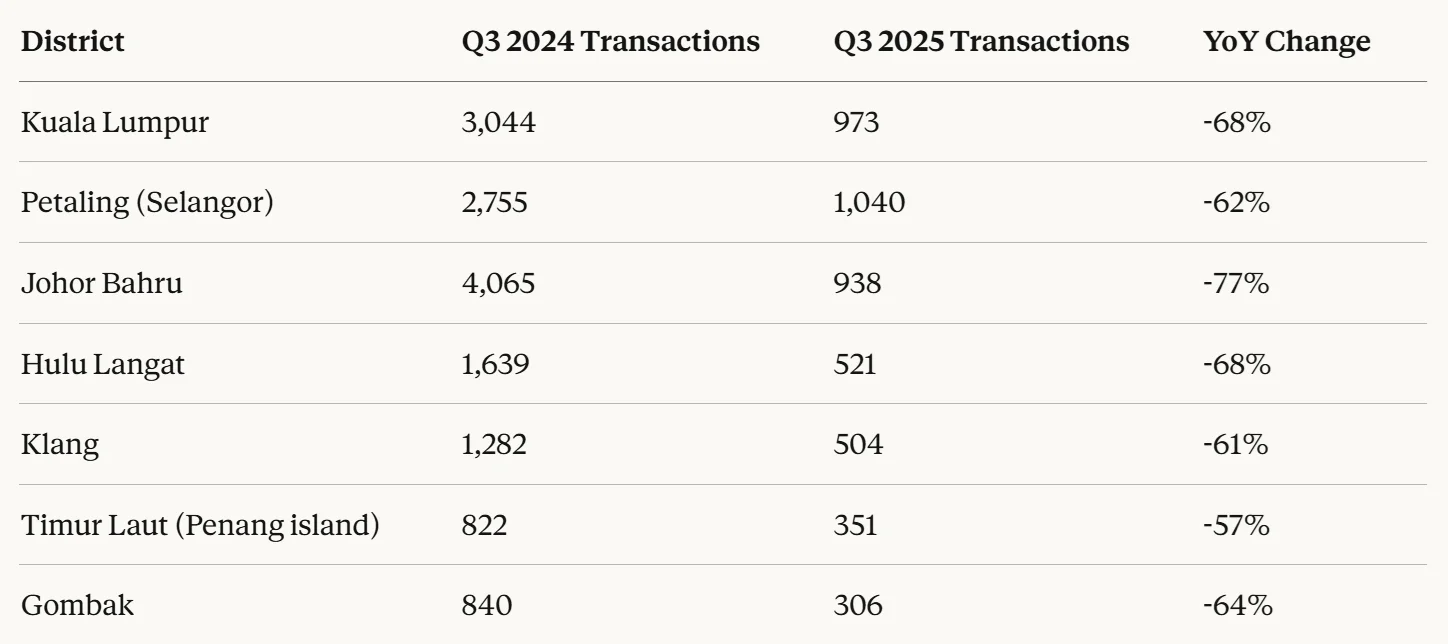

Property transaction counts fell 57–77% year-on-year across every major district in Q3 2025, compared to Q3 2024. The decline is consistent, simultaneous, and corroborated by developer survey data. This is not a data artefact.

The drop began simultaneously across unrelated markets in Q4 2024 — a pattern that points to a demand-side shock rather than localised problems.

NAPIC Q3 2025 figures may be revised upward as late registrations are finalised. However, the direction and scale of the decline is corroborated by developer survey data and is treated here as reflecting genuine market conditions.

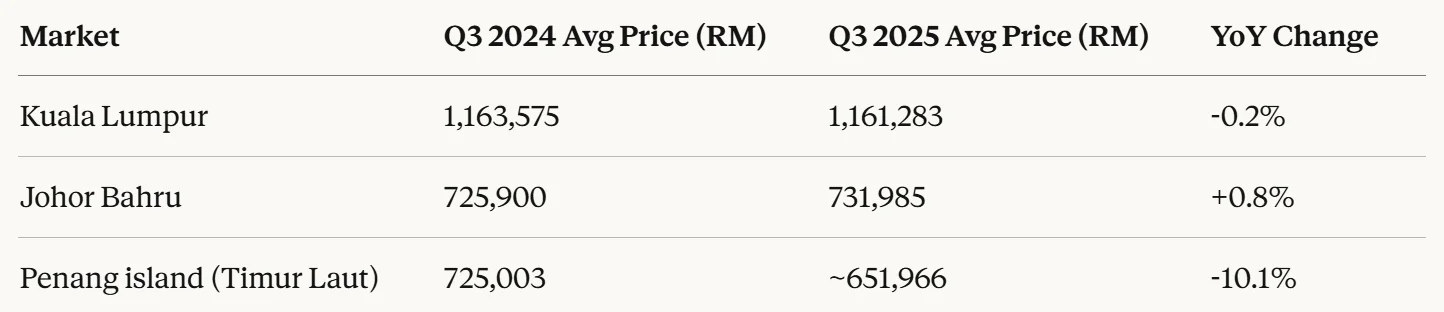

Despite the volume collapse, average transaction prices have been largely stable. Sellers are not yet adjusting on price.

KL and JB prices are effectively flat year-on-year. Penang island has softened around 10%. The gap between falling transaction volumes and stable headline prices is the defining tension in the market right now. Prices tend to lag volumes — and a market where fewer people can transact is not a market heading toward meaningful appreciation.

Rehda Malaysia's H2 2025 Property Industry Survey, released March 2026 and covering 166 developers, is unambiguous: 72% of developers reported that buyers could not secure mortgage approval.

The hardest-hit price band is homes between RM500,001 and RM700,000, where 31–45% of attempted transactions failed to get a loan approved. The main causes are high existing debt commitments and inconsistent income documentation, particularly among self-employed and gig economy buyers.

New launch take-up rates collapsed from 38% in H1 2025 to just 21% in H2 2025 — a drop that mirrors the volume decline in NAPIC transaction data. 60% of developers were holding unsold completed units as of December 2025. The national residential overhang reached 28,672 units in Q3 2025, up 30.5% year-on-year, worth RM17.25 billion. Add in unsold serviced apartments and the combined overhang exceeds 44,700 units. Condominiums and serviced apartments account for over half.

Budget 2026 has responded by doubling the Housing Credit Guarantee Scheme from RM10 billion to RM20 billion, targeting buyers outside standard bank lending criteria. Stamp duty exemptions for first-time buyers on homes up to RM500,000 have been extended through December 2027.

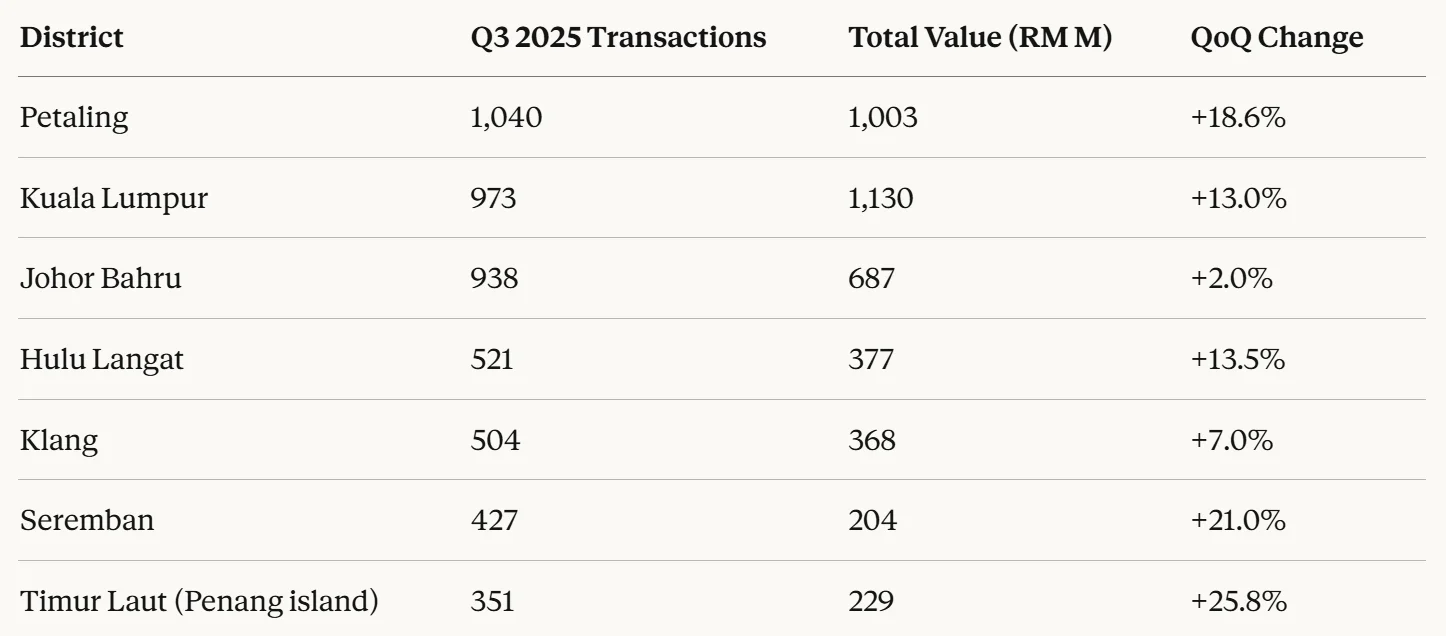

Within a broadly weaker market, some districts posted meaningful sequential recoveries quarter-on-quarter in Q3 2025.

Petaling and KL together accounted for over RM2.1 billion in a single quarter — the market's clearest concentration of active demand. Seremban's 22.5% value gain quarter-on-quarter makes it the standout second-tier market. Penang island's +40.2% QoQ value recovery is encouraging, though it needs to be read against a YoY decline of 57% in volume.

JB's split — volume barely up (+2% QoQ) but total transaction value down 12.4% — points to price pressure building in the mix even as units continue changing hands.

Johor received RM110 billion in approved investments in 2025 — the highest ever recorded by any Malaysian state. Singapore and China were effectively tied as the largest investors at ~RM58 billion each. Data centres from Microsoft, Equinix, and Princeton Digital Group are transforming industrial corridors in Kulai and Pasir Gudang.

The Johor-Singapore Rapid Transit System is 93% complete on the Malaysian side.

Parliament passed the RTS Link Bill on 12 February 2026, establishing the legal framework for co-located immigration. Fares are set at RM15.50–21.70 per journey. Commercial operations are targeted for January 2027.

Properties within 5 kilometres of planned RTS stations have already appreciated 18–20% in anticipation. JB city centre values have risen 40–50% since 2020. Rental yields in RTS-adjacent areas reach 6–8%.

In the near term, JB carries Malaysia's highest residential overhang by value at RM2.83 billion, concentrated in condominiums. Transaction volumes are down 77% year-on-year. Landed property near infrastructure nodes is significantly outperforming high-rise stock.

One important Q1 2026 update: the JS-SEZ master plan launch — originally scheduled for 30 March 2026 — was postponed following a Cabinet meeting in mid-March. No new date has been announced. The incentive framework remains operational, but the formal master plan delay introduces some planning uncertainty.

Three geopolitical developments in Q1 2026 are reshaping the risk environment.

The Iran conflict. On 28 February 2026, US and Israeli strikes killed Iran's Supreme Leader, triggering retaliation and a Strait of Hormuz crisis. Commercial traffic through the Strait dropped 81%. Brent crude surpassed $100 on 8 March and peaked near $126/barrel. Construction material costs — steel, aluminium, cement — are rising in response.

For Malaysia, this cuts both ways. As a net energy exporter, higher oil prices boost government revenue. But Budget 2026 assumed $60–65/barrel oil, and the monthly fuel subsidy bill has ballooned from RM700 million to RM4 billion. Construction cost inflation is a genuine near-term risk for developers.

US tariffs. The US Supreme Court ruled in February that Trump's original reciprocal tariffs were unconstitutional. A uniform 10% tariff replaced them, and Malaysia — which had negotiated its rate down from 25% — declared its bilateral trade deal null and void in March. Two new US trade investigations targeting Malaysia were launched in Q1, with potential escalation before July 2026.

The silver lining: safe-haven capital flows. JPMorgan's March assessment positioned Malaysia and China as the two Asian economies least vulnerable to the energy shock. Foreign equity inflows turned positive at +RM1 billion year-to-date by February — reversing RM5.15 billion in net outflows from 2025. Bank Negara projects 2026 GDP growth of 4–5%, maintaining its upgrade despite the Iran uncertainty.

From 1 January 2026, stamp duty on residential purchases by foreign nationals doubled from 4% to 8%. On an RM1.5 million property, that adds roughly RM75,000 to upfront costs. Total acquisition costs for foreign buyers — stamp duty, legal fees, and agency commissions — now run approximately 9–10% of purchase price.

State-level minimum purchase prices apply: RM1 million for strata properties in KL, Johor, and Penang island. Parts of Selangor require RM2 million.

Despite the cost increase, foreign demand has not pulled back meaningfully. In H1 2025, Chinese buyers led with 329 transactions worth RM834 million, followed by Singaporean buyers at 320 transactions worth RM518 million. Over 40% of JB city centre enquiries come from Singaporean buyers. MM2H now mandates property purchase across all tiers, creating structural demand.

Compared to Singapore's 60% Additional Buyer's Stamp Duty for foreign purchasers, Malaysia's 8% remains modest. For Singaporean buyers, JB condos at RM1,000–1,300 per square foot are 70–80% cheaper than comparable Singapore properties — and the current SGD/MYR exchange rate of approximately 3.11 amplifies the purchasing power differential.

Malaysia's property market is under genuine demand-side pressure. Transaction volumes are down sharply, unsold stock is building, and loan rejections are blocking a significant share of would-be buyers. Prices have held for now — but a market where fewer people can transact is not a market building toward meaningful appreciation.

The clearest opportunities remain in landed property with specific infrastructure catalysts — particularly within the Johor-Singapore SEZ corridor and near the RTS Link alignment. The most at-risk segment is high-rise condominiums in locations without a demonstrable demand anchor.

If you are buying for your own stay, current conditions — stable interest rates, reduced buyer competition, more negotiable sellers — are arguably the most favourable in several years. If you are buying purely as an investment, the data suggests patience and location selectivity matter more than timing the market right now.

The global geopolitical environment adds a layer of caution that was not there six months ago. But Malaysia's fundamental position — strong growth, stable rates, a transformative infrastructure pipeline, and regional safe-haven status — remains intact.

Speak to a registered estate negotiator (REN) before committing. Browse verified listings by price and location at the [MyRumahBaru property map].

[Johor's property market and what the JS-SEZ means for buyers]

[NAPIC 1H 2025: Malaysia's property market at a crossroads]

[Find verified property agents across Malaysia]

Q: Is the Malaysian property market slowing down in 2026? A: Yes, meaningfully. Transaction volumes across all major markets fell 57–77% year-on-year in Q3 2025 compared to Q3 2024. New launch take-up rates fell to 21% in H2 2025. Prices have remained broadly stable but demand-side pressures — particularly around mortgage access — are real and ongoing.

Q: How is the Iran conflict affecting Malaysian property? A: Malaysia is a net energy exporter, so higher oil prices generate fiscal upside. But construction material costs are rising, the fuel subsidy bill has surged, and global uncertainty is dampening investor sentiment. Bank Negara has flagged the conflict as the primary downside risk to its 4–5% GDP growth forecast for 2026, while maintaining that Malaysia is better positioned than most regional peers.

Q: Can foreigners buy property in Malaysia in 2026? A: Yes, subject to a minimum purchase price of RM1 million in most major states. From 1 January 2026, stamp duty of 8% applies to all residential purchases by non-citizens — doubled from the previous 4%.

Q: Which area in Malaysia has the most active property market right now? A: By total transaction value, Petaling and Kuala Lumpur lead, together accounting for over RM2.1 billion in Q3 2025. Johor Bahru has the strongest long-term infrastructure story. Seremban is the standout second-tier market with consistent QoQ value gains.

Q: Why are property transaction volumes down so sharply? A: The primary driver is financing access. Nearly three-quarters of developers reported buyers could not secure mortgage approval in H2 2025, particularly in the RM500,000–RM700,000 band. High household debt levels — RM1.65 trillion nationally, approximately 84.3% of GDP — and inconsistent income documentation among self-employed buyers are the main barriers lenders are citing.

Q: Is now a good time to buy property in Malaysia? A: For owner-occupiers, the conditions are relatively favourable — stable rates, lower competition, and sellers with more room to negotiate. For investors seeking capital appreciation, the current data suggests limited near-term upside in most segments. Landed property with a specific infrastructure catalyst is the clearest exception. Always consult a licensed REN and financial advisor before committing.

Written by MRB Editorial Team | Sources: NAPIC Property Market Report 2025 (released March 2026); Rehda Malaysia Property Industry Survey H2 2025; Bank Negara Malaysia Annual Report 2025; DOSM; Ministry of Finance Malaysia |

This is not a market in freefall. But it is a market under real, structural pressure. Here is what the data shows.

The Economy Is Strong. The Property Market Is Not Keeping Up.

Malaysia's GDP grew 6.3% in Q4 2025 — the strongest quarter in three years — and full-year 2025 growth came in at 5.2%, beating the government's own forecast. Unemployment fell to 2.9%, a decade low. The ringgit strengthened to its best level against the US dollar since 2018.

Bank Negara Malaysia held the Overnight Policy Rate at 2.75% through both its January and March 2026 meetings. Home loan rates for well-qualified buyers sit at 4.22–4.50% for conventional financing, and 3.95–4.15% for Islamic home loans. Inflation remains subdued at 1.4% as of February 2026.

On paper, these are conditions that should support a healthy property market. The friction is structural, not macroeconomic.

What NAPIC's 2025 Numbers Actually Show

The full-year 2025 NAPIC Property Market Report, released on 19 March 2026, confirmed that Malaysia's property market delivered value growth but volume decline. Total transaction value rose to RM241.87 billion — up 4.1% — on 416,413 transactions, down 1% year-on-year.

That headline figure, however, masks diverging trends. The national house price index grew just 2.6% for the full year, with the average transaction price reaching RM502,922. But by Q3 2025, the index had slipped 1.46% quarter-on-quarter — the first such quarterly decline since Q3 2021. Adjusted for inflation, house prices fell in real terms.

The segment driving headline value growth was industrial property, which surged 21.3% in value — powered by data centre land deals and logistics demand. Residential property, which most Malaysians actually care about, told a different story.

Transaction Volumes Fell Sharply — and the Drop Is Real

Property transaction counts fell 57–77% year-on-year across every major district in Q3 2025, compared to Q3 2024. The decline is consistent, simultaneous, and corroborated by developer survey data. This is not a data artefact.

The drop began simultaneously across unrelated markets in Q4 2024 — a pattern that points to a demand-side shock rather than localised problems.

NAPIC Q3 2025 figures may be revised upward as late registrations are finalised. However, the direction and scale of the decline is corroborated by developer survey data and is treated here as reflecting genuine market conditions.

Prices Are Holding — But Barely

Despite the volume collapse, average transaction prices have been largely stable. Sellers are not yet adjusting on price.

KL and JB prices are effectively flat year-on-year. Penang island has softened around 10%. The gap between falling transaction volumes and stable headline prices is the defining tension in the market right now. Prices tend to lag volumes — and a market where fewer people can transact is not a market heading toward meaningful appreciation.

Loan Rejections Are the Biggest Brake

Rehda Malaysia's H2 2025 Property Industry Survey, released March 2026 and covering 166 developers, is unambiguous: 72% of developers reported that buyers could not secure mortgage approval.

The hardest-hit price band is homes between RM500,001 and RM700,000, where 31–45% of attempted transactions failed to get a loan approved. The main causes are high existing debt commitments and inconsistent income documentation, particularly among self-employed and gig economy buyers.

New launch take-up rates collapsed from 38% in H1 2025 to just 21% in H2 2025 — a drop that mirrors the volume decline in NAPIC transaction data. 60% of developers were holding unsold completed units as of December 2025. The national residential overhang reached 28,672 units in Q3 2025, up 30.5% year-on-year, worth RM17.25 billion. Add in unsold serviced apartments and the combined overhang exceeds 44,700 units. Condominiums and serviced apartments account for over half.

Budget 2026 has responded by doubling the Housing Credit Guarantee Scheme from RM10 billion to RM20 billion, targeting buyers outside standard bank lending criteria. Stamp duty exemptions for first-time buyers on homes up to RM500,000 have been extended through December 2027.

Where Transactions Are Still Happening

Within a broadly weaker market, some districts posted meaningful sequential recoveries quarter-on-quarter in Q3 2025.

Petaling and KL together accounted for over RM2.1 billion in a single quarter — the market's clearest concentration of active demand. Seremban's 22.5% value gain quarter-on-quarter makes it the standout second-tier market. Penang island's +40.2% QoQ value recovery is encouraging, though it needs to be read against a YoY decline of 57% in volume.

JB's split — volume barely up (+2% QoQ) but total transaction value down 12.4% — points to price pressure building in the mix even as units continue changing hands.

Johor Bahru: The Long-Term Case and the Near-Term Reality

Johor received RM110 billion in approved investments in 2025 — the highest ever recorded by any Malaysian state. Singapore and China were effectively tied as the largest investors at ~RM58 billion each. Data centres from Microsoft, Equinix, and Princeton Digital Group are transforming industrial corridors in Kulai and Pasir Gudang.

The Johor-Singapore Rapid Transit System is 93% complete on the Malaysian side.

Parliament passed the RTS Link Bill on 12 February 2026, establishing the legal framework for co-located immigration. Fares are set at RM15.50–21.70 per journey. Commercial operations are targeted for January 2027.

Properties within 5 kilometres of planned RTS stations have already appreciated 18–20% in anticipation. JB city centre values have risen 40–50% since 2020. Rental yields in RTS-adjacent areas reach 6–8%.

In the near term, JB carries Malaysia's highest residential overhang by value at RM2.83 billion, concentrated in condominiums. Transaction volumes are down 77% year-on-year. Landed property near infrastructure nodes is significantly outperforming high-rise stock.

One important Q1 2026 update: the JS-SEZ master plan launch — originally scheduled for 30 March 2026 — was postponed following a Cabinet meeting in mid-March. No new date has been announced. The incentive framework remains operational, but the formal master plan delay introduces some planning uncertainty.

The Global Picture Is Adding Uncertainty

Three geopolitical developments in Q1 2026 are reshaping the risk environment.

The Iran conflict. On 28 February 2026, US and Israeli strikes killed Iran's Supreme Leader, triggering retaliation and a Strait of Hormuz crisis. Commercial traffic through the Strait dropped 81%. Brent crude surpassed $100 on 8 March and peaked near $126/barrel. Construction material costs — steel, aluminium, cement — are rising in response.

For Malaysia, this cuts both ways. As a net energy exporter, higher oil prices boost government revenue. But Budget 2026 assumed $60–65/barrel oil, and the monthly fuel subsidy bill has ballooned from RM700 million to RM4 billion. Construction cost inflation is a genuine near-term risk for developers.

US tariffs. The US Supreme Court ruled in February that Trump's original reciprocal tariffs were unconstitutional. A uniform 10% tariff replaced them, and Malaysia — which had negotiated its rate down from 25% — declared its bilateral trade deal null and void in March. Two new US trade investigations targeting Malaysia were launched in Q1, with potential escalation before July 2026.

The silver lining: safe-haven capital flows. JPMorgan's March assessment positioned Malaysia and China as the two Asian economies least vulnerable to the energy shock. Foreign equity inflows turned positive at +RM1 billion year-to-date by February — reversing RM5.15 billion in net outflows from 2025. Bank Negara projects 2026 GDP growth of 4–5%, maintaining its upgrade despite the Iran uncertainty.

What Foreign Buyers Need to Know

From 1 January 2026, stamp duty on residential purchases by foreign nationals doubled from 4% to 8%. On an RM1.5 million property, that adds roughly RM75,000 to upfront costs. Total acquisition costs for foreign buyers — stamp duty, legal fees, and agency commissions — now run approximately 9–10% of purchase price.

State-level minimum purchase prices apply: RM1 million for strata properties in KL, Johor, and Penang island. Parts of Selangor require RM2 million.

Despite the cost increase, foreign demand has not pulled back meaningfully. In H1 2025, Chinese buyers led with 329 transactions worth RM834 million, followed by Singaporean buyers at 320 transactions worth RM518 million. Over 40% of JB city centre enquiries come from Singaporean buyers. MM2H now mandates property purchase across all tiers, creating structural demand.

Compared to Singapore's 60% Additional Buyer's Stamp Duty for foreign purchasers, Malaysia's 8% remains modest. For Singaporean buyers, JB condos at RM1,000–1,300 per square foot are 70–80% cheaper than comparable Singapore properties — and the current SGD/MYR exchange rate of approximately 3.11 amplifies the purchasing power differential.

Key Numbers at a Glance

The Bottom Line

Malaysia's property market is under genuine demand-side pressure. Transaction volumes are down sharply, unsold stock is building, and loan rejections are blocking a significant share of would-be buyers. Prices have held for now — but a market where fewer people can transact is not a market building toward meaningful appreciation.

The clearest opportunities remain in landed property with specific infrastructure catalysts — particularly within the Johor-Singapore SEZ corridor and near the RTS Link alignment. The most at-risk segment is high-rise condominiums in locations without a demonstrable demand anchor.

If you are buying for your own stay, current conditions — stable interest rates, reduced buyer competition, more negotiable sellers — are arguably the most favourable in several years. If you are buying purely as an investment, the data suggests patience and location selectivity matter more than timing the market right now.

The global geopolitical environment adds a layer of caution that was not there six months ago. But Malaysia's fundamental position — strong growth, stable rates, a transformative infrastructure pipeline, and regional safe-haven status — remains intact.

Speak to a registered estate negotiator (REN) before committing. Browse verified listings by price and location at the [MyRumahBaru property map].

Related Reading

[Johor's property market and what the JS-SEZ means for buyers]

[NAPIC 1H 2025: Malaysia's property market at a crossroads]

[Find verified property agents across Malaysia]

Frequently Asked Questions

Q: Is the Malaysian property market slowing down in 2026? A: Yes, meaningfully. Transaction volumes across all major markets fell 57–77% year-on-year in Q3 2025 compared to Q3 2024. New launch take-up rates fell to 21% in H2 2025. Prices have remained broadly stable but demand-side pressures — particularly around mortgage access — are real and ongoing.

Q: How is the Iran conflict affecting Malaysian property? A: Malaysia is a net energy exporter, so higher oil prices generate fiscal upside. But construction material costs are rising, the fuel subsidy bill has surged, and global uncertainty is dampening investor sentiment. Bank Negara has flagged the conflict as the primary downside risk to its 4–5% GDP growth forecast for 2026, while maintaining that Malaysia is better positioned than most regional peers.

Q: Can foreigners buy property in Malaysia in 2026? A: Yes, subject to a minimum purchase price of RM1 million in most major states. From 1 January 2026, stamp duty of 8% applies to all residential purchases by non-citizens — doubled from the previous 4%.

Q: Which area in Malaysia has the most active property market right now? A: By total transaction value, Petaling and Kuala Lumpur lead, together accounting for over RM2.1 billion in Q3 2025. Johor Bahru has the strongest long-term infrastructure story. Seremban is the standout second-tier market with consistent QoQ value gains.

Q: Why are property transaction volumes down so sharply? A: The primary driver is financing access. Nearly three-quarters of developers reported buyers could not secure mortgage approval in H2 2025, particularly in the RM500,000–RM700,000 band. High household debt levels — RM1.65 trillion nationally, approximately 84.3% of GDP — and inconsistent income documentation among self-employed buyers are the main barriers lenders are citing.

Q: Is now a good time to buy property in Malaysia? A: For owner-occupiers, the conditions are relatively favourable — stable rates, lower competition, and sellers with more room to negotiate. For investors seeking capital appreciation, the current data suggests limited near-term upside in most segments. Landed property with a specific infrastructure catalyst is the clearest exception. Always consult a licensed REN and financial advisor before committing.

Written by MRB Editorial Team | Sources: NAPIC Property Market Report 2025 (released March 2026); Rehda Malaysia Property Industry Survey H2 2025; Bank Negara Malaysia Annual Report 2025; DOSM; Ministry of Finance Malaysia |