Why So Many Malaysians Can't Get a Home Loan in 2026

timer

4 minutes read

June 30, 2026

Developers launched more homes in the second half of 2025 than they did in the first half. They sold far fewer. That gap is the whole story of the property market right now.

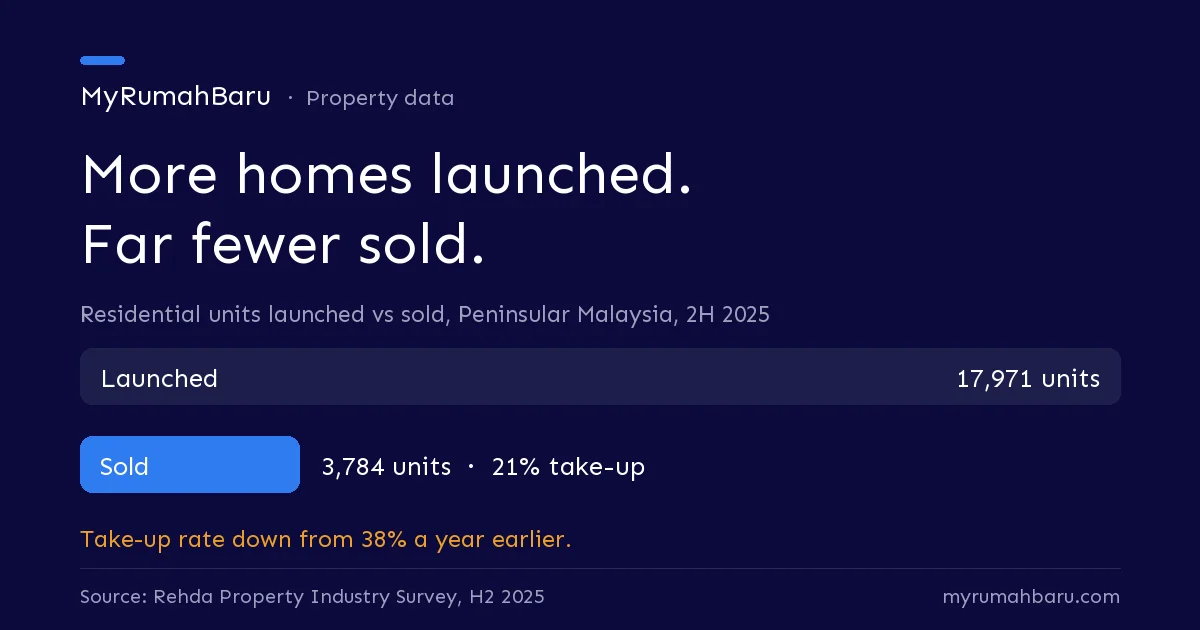

Rehda's latest [Property Industry Survey], covering 166 developers across Peninsular Malaysia, put real numbers to it. 17,971 residential units were launched in 2H 2025. Only 3,784 were sold. That is a take-up rate of 21%, down from 38% in the first half of the year.

So why didn't the rest sell? 72% of developers pointed to the same thing: financing. Not price. Not lack of interest. Buyers wanted the homes but could not get the loan to pay for them. The deals are dying at end-financing, the housing loan a buyer needs to actually complete the purchase. It lines up with what [the wider data has been telling us]: a market where fewer people can transact, not one running out of homes.

Here is what makes this market different. Borrowing is not expensive right now. Bank Negara has [held the OPR at 2.75%] since the July 2025 cut, and inflation stayed low at 1.6% in the first quarter of 2026.

So the rejections are not about high interest. They are about affordability and risk. Banks are looking harder at your debt service ratio (DSR), your CCRIS and CTOS records, and how stable your income really is. A payslip is no longer enough. The squeeze is worst in the RM500,001 to RM700,000 band, which is exactly where most first-home and upgrader stock sits.

If you are a first-time buyer. Get your loan sorted before you fall in love with a unit. The first-timer stamp duty exemption on homes up to RM500,000 has been extended to 2027, which helps your upfront cost. It does nothing for the loan itself. Your DSR does.

If you are upgrading. Your car loan, your existing mortgage, your PTPTN all count against you. Clear what you can before you apply, not after the bank says no.

If you are selling. A buyer with a signed SPA but no approved loan is not a sale. Ask about financing early. It is the difference between a closed deal and three wasted months.

If you are a developer. This is already in your numbers, and it is part of the [growing overhang of unsold completed homes]. Bridging finance is tighter too, with banks now asking for 30% to 60% sales thresholds before drawdown. Pricing to the band that can actually get funded matters more than launching more units.

Check your DSR before you start shopping, not after.

Pull your CCRIS and CTOS reports and fix any surprises.

Get an Approval-in-Principle from a bank first.

Shop within the loan you can actually get, not the price you are hoping for.

We will be honest: no property portal can get your loan approved. That is between you and the bank. What we can do is stop you wasting months chasing a home the bank was never going to fund. We show area-level prices and [real, verified data] so you start from what you can borrow, then look. That is the right order.

Start with your number. Then find the home that fits it. You can browse by price and location on the [MyRumahBaru map].

Not only your salary. Banks look at your DSR, which weighs all your monthly commitments against your income, plus your CCRIS and CTOS credit records. A good salary with heavy existing debt can still be rejected.

No. A lower OPR makes repayments cheaper, but it does not change how strict the bank is on approval. In 2026, rates are low and approvals are still tight.

It depends on your net income after commitments and your DSR limit, not the property price. Get an Approval-in-Principle before you shop so you know your real ceiling.

Homes are being launched, but only 21% are selling. The blocker is financing, not demand.

Low interest rates are not helping. Approval is about DSR and credit, not the OPR.

Sort your loan eligibility before you shop, especially in the RM500k to RM700k band.

[Malaysia Property Overhang 2026: Why Homes Aren't Selling]

[Malaysia Property Market 2026: What the Data Is Really Telling Us]

[NAPIC Q1 2026: What Malaysia's Property Data Means for Buyers]

Written by MyRumahBaru Editorial Team. Sources: Rehda Property Industry Survey (H2 2025); Bank Negara Malaysia Monetary Policy Statement, 7 May 2026. Last reviewed June 2026.

Rehda's latest [Property Industry Survey], covering 166 developers across Peninsular Malaysia, put real numbers to it. 17,971 residential units were launched in 2H 2025. Only 3,784 were sold. That is a take-up rate of 21%, down from 38% in the first half of the year.

So why didn't the rest sell? 72% of developers pointed to the same thing: financing. Not price. Not lack of interest. Buyers wanted the homes but could not get the loan to pay for them. The deals are dying at end-financing, the housing loan a buyer needs to actually complete the purchase. It lines up with what [the wider data has been telling us]: a market where fewer people can transact, not one running out of homes.

The strange part: money is cheap, but loans still get rejected

Here is what makes this market different. Borrowing is not expensive right now. Bank Negara has [held the OPR at 2.75%] since the July 2025 cut, and inflation stayed low at 1.6% in the first quarter of 2026.

So the rejections are not about high interest. They are about affordability and risk. Banks are looking harder at your debt service ratio (DSR), your CCRIS and CTOS records, and how stable your income really is. A payslip is no longer enough. The squeeze is worst in the RM500,001 to RM700,000 band, which is exactly where most first-home and upgrader stock sits.

What this means for you

If you are a first-time buyer. Get your loan sorted before you fall in love with a unit. The first-timer stamp duty exemption on homes up to RM500,000 has been extended to 2027, which helps your upfront cost. It does nothing for the loan itself. Your DSR does.

If you are upgrading. Your car loan, your existing mortgage, your PTPTN all count against you. Clear what you can before you apply, not after the bank says no.

If you are selling. A buyer with a signed SPA but no approved loan is not a sale. Ask about financing early. It is the difference between a closed deal and three wasted months.

If you are a developer. This is already in your numbers, and it is part of the [growing overhang of unsold completed homes]. Bridging finance is tighter too, with banks now asking for 30% to 60% sales thresholds before drawdown. Pricing to the band that can actually get funded matters more than launching more units.

What to do now

Check your DSR before you start shopping, not after.

Pull your CCRIS and CTOS reports and fix any surprises.

Get an Approval-in-Principle from a bank first.

Shop within the loan you can actually get, not the price you are hoping for.

Where we stand

We will be honest: no property portal can get your loan approved. That is between you and the bank. What we can do is stop you wasting months chasing a home the bank was never going to fund. We show area-level prices and [real, verified data] so you start from what you can borrow, then look. That is the right order.

Start with your number. Then find the home that fits it. You can browse by price and location on the [MyRumahBaru map].

Is my home loan getting rejected because of my salary?

Not only your salary. Banks look at your DSR, which weighs all your monthly commitments against your income, plus your CCRIS and CTOS credit records. A good salary with heavy existing debt can still be rejected.

Does a lower OPR mean it is easier to get a loan?

No. A lower OPR makes repayments cheaper, but it does not change how strict the bank is on approval. In 2026, rates are low and approvals are still tight.

What loan amount can I actually get approved for?

It depends on your net income after commitments and your DSR limit, not the property price. Get an Approval-in-Principle before you shop so you know your real ceiling.

Key takeaways

Homes are being launched, but only 21% are selling. The blocker is financing, not demand.

Low interest rates are not helping. Approval is about DSR and credit, not the OPR.

Sort your loan eligibility before you shop, especially in the RM500k to RM700k band.

Related reading

[Malaysia Property Overhang 2026: Why Homes Aren't Selling]

[Malaysia Property Market 2026: What the Data Is Really Telling Us]

[NAPIC Q1 2026: What Malaysia's Property Data Means for Buyers]

Written by MyRumahBaru Editorial Team. Sources: Rehda Property Industry Survey (H2 2025); Bank Negara Malaysia Monetary Policy Statement, 7 May 2026. Last reviewed June 2026.